4,99 €

Mehr erfahren.

- Herausgeber: Ullstein Ebooks in Ullstein Buchverlage

- Kategorie: Sachliteratur, Reportagen, Biografien

- Sprache: Englisch

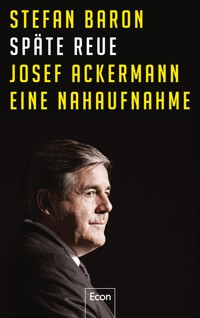

He was in the cross-fire of public criticism like no other top executive in Germany. Josef Ackermann, CEO of the Deutsche Bank until 2012, can look back over turbulent times. His 'V for victory' sign and his return-on-equity target of 25 percent, made him, for many, the bad guy of the nation. The role he played in the financial crisis is also controversial. Was he one of those who caused the misery, or did he mitigate the crisis and act as a decisive force in overcoming it? Stefan Baron, head of communications at Deutsche Bank during the crisis, paints a fascinating and up-close portrait of Josef Ackermann. Few are better placed to describe his convictions, his strengths and his weaknesses. From his uniquely close vantage point, Baron describes the way Ackermann and his attitudes changed during this epoch-making period.

Das E-Book können Sie in Legimi-Apps oder einer beliebigen App lesen, die das folgende Format unterstützen:

Veröffentlichungsjahr: 2014

Ähnliche

STEFAN BARON

LATE REMORSE

JOE ACKERMANN, DEUTSCHE BANK AND THE FINANCIAL CRISIS

Econ

Econ is a publishing house of

Ullstein Buchverlage GmbH

Translated edition

Translation by Mark Wilch

Cover design: Etwas Neues entsteht, Berlin

Photo on front cover: © Laif

ISBN 978-3-8437-1001-5

© by Ullstein Buchverlage GmbH, Berlin, Germany 2014

Contents

Cover

Front page

Impressum

Contents

Prologue:How it all began

Chapter 1Dancing As Long as the Music Plays

Chapter 2Stupid Germans

Chapter 3Destructive Creation

Chapter 4The Compass for Life

Chapter 5Knowledge and Interest

Chapter 6Staring into the Abyss

Chapter 7Between Triumph and Humility

Chapter 8The Worst Day

Chapter 9Spies and Cluster Bombs

Chapter 10The Battle for Succession

Chapter 11From Banker to Statesman

Chapter 12The Legacy

EpilogueTaking Stock

Author’s Note

Literature

Pictures

Plate

Prologue:How it all began

Josef Ackermann smiled his famous smile, shook my hand and said: “See you again in Frankfurt.” Before the CEO of Deutsche Bank, who had just hired me as his new global head of communications, left the coffee shop of the Steigenberger Park Hotel at the end of Düsseldorf’s Königsallee boulevard, he asked me if I could get the bill, as he had no cash on him.

Lucky for me, I thought, that I had put a couple of notes in my pockets that morning, although I don’t usually carry any cash myself. It was enough for the two cappuccinos and croissants we’d had. “No problem. I’ll see to it,” I answered, leaving Germany’s top banker free to head straight for the black, bullet-proof Mercedes S-class limousine waiting outside to whisk him off to his next appointment.

As I walked back to my office along the tree-lined “Kö”, which was showing the first signs of spring, I gradually realized what had just happened. At the age of 59, when many people enter early retirement, I had agreed to embark on the greatest adventure of my professional life. A passionate journalist, I had declined all offers to change sides for thirty years, but now, in less than an hour, agreed to manage communications for Germany’s most controversial company and most controversial executive.

Everything had gone so incredibly fast. Just two days before, an old acquaintance of mine had asked me out of the blue whether I would be interested in the position. More out of curiosity as to how seriously this was meant than anything else I had signalled interest in principle. It was dead serious, as I had realized only one day later when I was asked to meet Josef Ackermann the next morning for breakfast. Now I really had to give the idea some earnest thought.

Journalism has always been my favorite profession. But after serving 16 years as editor-in-chief of WirtschaftsWoche, Germany’s leading business magazine, the job had become a little humdrum. In addition, the deepening crisis of the print media was increasingly turning it into a rear guard battle – not a pleasant prospect for someone who had only known the offensive so far.

These feelings were reinforced by Deutsche Bank’s special appeal. Across the length and breadth of Germany, no company attracts even nearly as much public attention. Founded in Berlin in 1870 by ‘highest decree of his Majesty the King of Prussia’, the bank is not only the country’s premier financial institution and the only one with a really global scope, it is also Germany’s most important and most powerful company, a national institution with almost mythical status. Its CEO is widely seen as a kind of “shadow chancellor of the Republic”.

I felt close to the bank because of my many years as a customer, but even more because of the years I spent working as financial correspondent for Germany’s leading news magazine Der Spiegel in the second half of the nineteen-eighties, covering Deutsche. Just weeks before Alfred Herrhausen, the then chairman of the board, was murdered by a left wing terrorist group, the so-called Red Army Faction, I had written a cover story on him titled “The Lord of Money”. Not least for that reason, his death had touched me deeply.

At the time, globalisation, British prime minister Maggie Thatcher’s “big bang”, and the economic liberalization introduced by US president Ronald Reagan had ushered in the golden age of finance and the ascension of investment bankers to the position of “Masters of the Universe”. Those were exciting times for a young business journalist, and I always kept fond memories of them. The prospect of reconnecting to that time was also a factor in my late change of career.

Then, of course, there was an excellent pay package and above all – Josef Ackermann. Since his disastrous V for victory sign in a Düsseldorf courtroom, many Germans saw in him the chief villain of the nation.

In the spring of 2000, the British telecommunications giant Vodafone had taken over its German rival Mannesmann. Resistance there had been vehement, and the value of the company on the stock market had risen considerably in the process. As a reward, the members of the supervisory board’s top committee, among them the head of Deutsche Bank, authorized special bonuses of 57 million Deutschmarks for several top figures of the company.

A payment of that sort was nothing exceptional for Ackermann and the amount of money in question rather small by international standards. But the Düsseldorf state prosecutors were unimpressed by Anglo-Saxon customs. They accused the CEO of Deutsche Bank along with the other committee members of “a particularly serious case of embezzlement”, a crime that carries a jail sentence of up to ten years.

When the case opened at the Düsseldorf Regional Court on January 21, 2004 “probably the most misinterpreted press photo” in German business history was taken, as Rainer Hamm, a criminal lawyer involved in the case, put it. The judges were late to arrive in courtroom L111, and as the defendants waited, they passed the time with small talk. The conversation turned to the American pop star Michael Jackson. Five days earlier, at the start of his child molestation trial, Jackson had first kept the court waiting and then made the V for victory sign upon leaving. Josef Ackermann imitated the gesture as a joke and was caught on camera by a photographer of the German news agency dpa.

The image was soon all over the media and led to a storm of outrage in Germany. “Obscene” and “an abyss of arrogance” commented Süddeutsche Zeitung, a leading national daily. “Ackermann has lost, even if he wins the trial,” wrote Der Spiegel in a cover story titled ‘The Arrogance of the Powerful’.

The fatal misunderstanding could conceivably have been cleared up by a swift public explanation from Ackermann. But his comments as he left the courtroom later describing Germany as “the only country where those responsible for creating value are punished” made this impossible. Those comments, wrote Süddeutsche Zeitung, show the Deutsche Bank CEO’s contempt for all those who “create value by working hard for little pay”. Overnight, Josef Ackermann had become the ugly face of capitalism in Germany. His acquittal in late November 2006, almost three years later, in return for a payment of 3.2 million euros, did not help much to improve that image.

It could not get any worse, I thought, when pondering whether to accept Ackermann’s offer. The only direction his popularity rating could go was up. Not a bad starting point to take on a communications job.

What’s more, Josef Ackermann and I have much in common. We are the same age, almost to the day (I am one day older), and we both grew up in small, rural communities, which had once been prosperous but then suffered from profound structural change during our youth, due to the precursors of globalisation. We were both brought up by strict but loving parents from the Catholic middle class who taught us to be ambitious, industrious and open-minded and take responsibility for our actions. Having learned Latin and classical Greek in high school and studied economics, we also received the same education. In short: We had a natural understanding between us that did not require many words. That tipped the scales and finally made me change sides.

A story in WirtschaftsWoche in August 2000 had led to Josef Ackermann’s early nomination as the next head of Deutsche Bank, almost two years before the term of his predecessor, Rolf-Ernst Breuer, was over. Dirk Schütz, a colleague of mine, had reported that Thomas Fischer, a fellow board member of the Swiss national, also harbored great ambitions to get the top job at Deutsche.

Ackermann must have been alarmed by the story. His hopes of becoming number one had already been destroyed once before at SKA (Schweizerische Kreditanstalt), today Credit Suisse, his former employer, and he had left the bank for Deutsche. He didn’t want to go through such a sad experience again.

The WirtschaftsWoche-story also stirred up Deutsche’s investment bankers in London around Edson Mitchell, head of securities trading. They wanted to see someone leading the bank who understands and wholeheartedly supports them and their business. Their only candidate was Josef Ackermann. After the summer break they forced a debate on Breuer’s succession. Most management board members feared this debate would drag on for two years and Tessen von Heydebreck, the most senior among them, proposed to take a vote right away. The board, Fischer included, voted for Ackermann as their next leader. Fischer later took the helm at WestLB, then Germany’s largest regional bank.

Up until our breakfast at Park Hotel, Josef Ackermann and I had seen each other a few times only. I remember a short meeting in November 2003 at a welcome party for Jean-Claude Trichet, the new head of the European Central Bank (ECB), at Schlosshotel Kronberg near Frankfurt. We had some small talk after dinner, but that was it.

The next time we had met on a weekend at the end of March 2005 in still snowed-in Kitzbühel in the Tyrolean Alps. The Holtzbrinck publishing group, to which WirtschaftsWoche belongs, had invited him as special guest to its annual top leadership meeting. To our great surprise, the head of mighty Deutsche Bank had arrived all alone without entourage and readily joined in the heavy drinking after dinner at Rosi’s Sonnbergstuben as well as in dancing the farewell polonaise at dusk.

Most vividly I recall our meeting for an interview in September of the same year in Deutsche Bank’s headquarters in Frankfurt. During the conversation, I had branded Ackermann’s opportunistic focus on the highly profitable investment business at the time a “let the good times roll” strategy and he had visibly liked that label. After the microphone was off we had chatted for a while on my studies of economics at Cologne University and my years at the Kiel Institute for World Economics. I had felt a common wavelength between us.

When Ackermann became “speaker” of the managing board of Deutsche Bank, as his position was still called in 2002, he wanted to be a banker pure and simple. His goal was to whip Deutsche, which at the time was barely making a profit with its own operations and in danger of being taken over back into shape; and to turn it from a traditional lender into a leading global investment bank. The bank’s political role in Germany – probably unparalleled anywhere in the world – and the large media interest it aroused in its home market were new to the first non-German at the helm of this venerable institution. In addition, with no network of personal connections in the country to rely on, he believed he needed to keep a low profile in public life. This had also been the advice from his consultants.

However, as the Mannesmann trial progressed, Ackermann increasingly realized he would have no choice but to accept the political mantle ascribed to the head of the Deutsche Bank in Germany, if he was to succeed in his job and earn the esteem of the people in the bank’s home market. He needed to foster closer connections there, to step up and reorient his communications. That’s where we met.

Once resolved to quit my job as editor-in-chief, I wanted to join Deutsche Bank at the earliest possible time. Stefan von Holtzbrinck, my employer, wasn’t amused about my decision, though, and balked at granting me that wish. Instead he insisted that I serve out my contract still running more than a full year. That would have been tantamount to the end of Josef Ackermann’s and my plans. It required a number of personal phone calls by the head of Deutsche Bank to end the publisher’s blockade.

And so, on June 1, 2007, my adventure at Deutsche began. It was to become so much greater than I could have ever imagined in my wildest dreams. At that time, I had not an inkling of the epochal crisis which was soon to shake the global financial system to its very foundations.

Once again, however, the old adage, ‘in every crisis there lies opportunity’, was to be proven correct. When Josef Ackermann was faced with the challenge of his life, he proved up to the task. The more the situation escalated, the more insecure and even panicky others grew, the calmer and more assured he became. I realized that here was a man who had his appointment with destiny.

Long before most of his global peers, this man from the Swiss countryside, who in the years before had literally boxed Deutsche Bank into the top flight of international investment banking with high leverage and ambitious return-on-equity targets, recognized the extent of the coming danger and acted accordingly. That way, he managed to steer his institution relatively unscathed through the crisis without taking taxpayers’ money and then re-aligned it to face a new future.

In addition he was the first among the world’s top bankers to publicly show remorse over what had gone wrong in his industry and his own institution. As chairman of the Institute of International Finance (IIF), the global association of financial institutions in Washington D.C., and therefore spokesman of his industry, he became the leading light of its reformers, campaigning for banks to resolutely re-focus on their customers, the real world, and their social tasks. He placed himself at the forefront of efforts to solve both the financial crisis and the European sovereign debt crisis, which came in its wake.

Surely, Ackermann’s remorse set in only after much of the damage had already been done. But isn’t it true for most of us, that the damage must first be done before we learn our lesson? And, what in hindsight might appear to have come late, too late even – for a leading banker it was early, very early indeed. And it was sincere, although not entirely motivated by selfless concerns.

At the annual general meeting of Deutsche Bank on May 31, 2012, Ackermann’s day of farewell, the more than 7000 shareholders present repeatedly rose to give him standing ovations – despite a clearly unsatisfactory share price, an ugly battle for succession, and a long list of legal disputes. During the years of crisis, the former bad guy of the German financial industry had morphed into “a world statesman”, as the German business daily Handelsblatt expressed it.

The present book aims to chart this remarkable metamorphosis, to explore the background against which it unfolded, the conditions that made it possible and its concomitant events and consequences. It is a tale of struggle and competition, triumph and frustration, glory and scandal, limelight and loneliness. It is a portrait of a man of his time, a multifaceted personality out of the ordinary, whose charisma leaves its impression even on his opponents. And it is a contribution to financial history and to the history of morality of the financial industry from a unique vantage point.

I remain close to Josef Ackermann and still advise him in matters of personal communications. This book is, however, not an authorized biography, but a personal account of my time working at his side; a close-up view of the defining years of his career.

Having been a journalist for many years, I am aware of the vital importance of maintaining a critical distance to one’s subject of description, however close one might feel to it. I kept that distance during my years at Deutsche Bank as well. It was to the benefit of both sides, I believe.

It remains for the reader to judge how well I have managed to achieve that goal in this book. “Every reality consists of two parts – a subject and an object. If the object is totally the same, but the subject different, the reality is therefore a different one as well,” the philosopher Arthur Schopenhauer wrote in his Aphorisms on the Wisdom of Life.

This book is my reality of Josef Ackermann.

Chapter 1Dancing As Long as the Music Plays

My start as communications director at Deutsche Bank becomes a baptism of fire. I have been in the twin towers, its landmark headquarters in Frankfurt, for only some weeks when the worst financial crisis since the 1930s breaks out. The European sovereign debt crisis follows in its wake. The world is still suffering from both today.

The outbreak of the crisis is marked in Germany by the near collapse of Industriekreditbank (IKB) in late July 2007. IKB was in the business of financing small and medium-sized enterprises and had been considered rock-solid, even boring, up to that point. The bank was founded in 1924 to handle German reparation payments from the First World War. Until the middle of the past decade, it had been located on Kasernenstraße in Düsseldorf, right across the street from Handelsblatt Group, the publishing house to which WirtschaftsWoche also belongs. The bank employees we saw walking in and out of the building and ran into at lunch in the local restaurants seemed so staid to us journalists that it would never have occurred to us, what was being cooked up in our immediate neigborhood.

BaFin, Germany’s financial supervisory authority based in Bonn, had not become suspicious either, but this failure doesn’t make matters any better. It still deeply troubles me today that we failed to detect what was going on in that building across the street and let ourselves be deceived by appearances and clichés.

Back in February 2004, Risk, a trade journal, had already run up a warning flag. In a three-page article titled “The Great German Structured Credit Experiment” it said: “IKB, the conservative moneylender for German mid-caps, has transformed itself into Germany’s biggest investor for structured credit products – with a penchant for riskier transactions.” That should have been enough of a warning to view our neighbors in a different light and to start questioning the entire banking system.

IKB’s annual report for 2006/2007 indicated the high risk the bank had taken on as well. One just had to take a close look at the document. On page 57 it said: “Other commitments comprise loan commitments to special purpose entities for a total equivalent of 8.1 billion euros.” The bank’s equity capital, for its part, totaled just 1.2 billion euros.

Later, when the crisis hit, and one earthquake after another shook the financial system, almost causing it to collapse, I asked myself time and again how so many economic and business media around the globe could have missed the story of the century. Why, with very few exceptions, we failed collectively as a profession and on the whole acted “more like a cheerleader than like a check” as the gigantic financial bubble grew before our eyes. That is at least how Joseph E. Stiglitz, Nobel Prize Laureate in Economics, describes the situation in his contribution to Bad News – How America’s Business Press Missed the Story of the Century, edited by Anya Schiffrin from Columbia University in New York.

Might the reason be that the media industry was and still is in the middle of a deep-reaching structural transformation and many media are fighting for their very survival in what is sometimes ruinous competition? Might that have been why there is not enough time left anymore for thorough research and for drawing sound conclusions based on it?

All too often, tossing out a quick opinion seems to be the only way out for journalists lacking the resources to independently collect facts. It is cheap and easy to produce but as easily forgotten by the readers. Or journalists may be tempted to become ‘embedded’ in the object of their observation to the detriment of their credibility. Both practices have serious consequences for the rationality and efficiency of our society. Democracy and the market economy, freedom of choice and the sovereignty of consumers are based on the ability of citizens and market participants to form a relatively accurate picture of reality.

In the years leading up to the financial crisis, that was clearly not the case. And yet there was no shortage of warning signs: There were the ever increasing imbalances in current accounts, particularly the huge US deficit and China’s gigantic surplus, the enormous capital inflow into America as a consequence, and cheap money. The financial sector, especially new types of largely opaque credit instruments and shadow banking, were expanding at an explosive speed. Bank balance sheets and government budgets became bloated with debt. Risk awareness receded with the securitization of loans. In the US, a big bubble in real estate was building, accompanied by a high level of private debt and poor lending standards for mortgage loans.

But all those warning signals – to name but the most visible ones – were disregarded. Not only by bankers, but also by those who were supposed to supervise them, i. e. supervisory boards and regulatory authorities, auditors and rating agencies – and likewise, with few exceptions, the media.

In February 2007, Maria Bartiromo (aka “Money Honey”), star host of the US commercial TV network CNBC, asked prominent corporate executives attending the World Economic Forum in the Swiss alpine village of Davos to designate the most important issue confronting them in the year just started. In her book on the financial crisis (The Weekend That Changed Wall Street) a few years later, she noted that Josef Ackermann was the only top manager to mention the strong debt overhang in the US real estate market as his gravest concern.

Later, after the crisis had broken out, Bartiromo asked the chief executive of Deutsche Bank whether he had seen the disaster coming. He honestly admitted: “We knew something but not much. I did not anticipate the financial crisis. In a booming economy, real estate bubbles and too much debt are always a problem.” Bubbles are “especially important when they coincide with high levels of debt,” was also Carmen M. Reinhart’s and Kenneth S. Rogoff’s main conclusion from their analysis of financial crises over the past 800 years (This Time is Different – Eight Centuries of Financial Folly).

Americans had never had an easier time buying a house on credit than after the traumatic terrorist attacks on the World Trade Center in New York on September 11, 2001. Without collateral, oftentimes even without income. Those loans became known as Ninja loans: “No income, no job, no assets.”

President George W. Bush had proclaimed the “Ownership Society” to keep the American people’s spirits up in spite of the terrorist attacks and the ensuing Iraq War. As long as real estate prices were rising and interest rates remained at one percent, the lax standards were no problem. The homes bought virtually paid for themselves. But in 2006 prices stopped rising because of the growing building glut. Then they began to fall here and there, especially in the subprime segment of financially weak buyers. At the same time interest rates started climbing. Foreclosures became more frequent; the bubble threatened to burst.

Things have not quite reached that point when I begin my job at Deutsche Bank. “As long as the music is playing, you’ve got to get up and dance,” Chuck Prince, Citibank CEO at the time, had quipped. His dictum is shared in private by my boss, Josef Ackermann: “If you withdraw too early from a business still going well, you forfeit profit, lose market share and possibly even your independence.”

In June 2007 the music is still playing. In the first quarter, Deutsche Bank had posted a profit of 3.2 billion euros before tax, a new record in its long history. One detail had remained largely ignored, however: 200 million euros of that profit came from Greg Lippmann, chief of asset-backed securities (ABS) trading in New York. Back in September 2005 his colleague, Eugene Xu, a PhD in mathematics from Shanghai, had already forecast that there would be an upsurge in bankruptcies among US homebuyers and related to that a steep fall in the prices of securities backed by subprime mortgage loans. Since then Lippmann had bet on the bubble bursting while colleagues still kept blowing it up. Now the man whom the New York Times later called the “Cassandra of the financial crisis” is progressively proven right.

Deutsche Bank CEO Josef Ackermann himself is feeling increasingly nervous with regard to the US subprime market but he does not envisage its collapse, let alone a crisis of the international financial system. His bank as a whole, in any case, does not bet on a downturn.

Why should it? Everything seems to be humming along so nicely. On Friday, June 3, 2007, the major German stock market index DAX hits 8,000 points, nearly its all-time high up to that juncture. The price of Deutsche Bank shares climb to a record 118 euros.

During my first two weeks in Frankfurt, I do not catch sight of my boss even once. Before I arrived, he had embarked on a long business trip. First to Athens to attend the spring meeting of the International Institute of Finance (IIF), the global association of the financial industry of which he is chairman. And from there half way around the globe to Cape Town, Paris, St. Petersburg, New York, Washington, and on to the West Coast of the US.

Josef Ackermann is at home in airplanes. Chicago in the morning, Houston at lunchtime, Las Vegas at dusk and Los Angeles in the late evening. He will dine on Wiener Schnitzel or beef tartare with journalists at Restaurant Borchardt in Berlin, then board a plane and have breakfast the next morning with a central banker in New York, a government minister in Mexico City or a key client in São Paulo. That is routine for the Deutsche CEO, as I was soon to find out. On a trip to South America, for instance, within the space of a week he sees the heads of government of Peru, Argentina and Brazil, one after the other.

Quite often Ackermann is also traveling on weekends. Once, he flies on Friday night from Frankfurt to China to attend a meeting of the international advisory board of the city of Shanghai and is back in his office early Monday morning. Another time, he travels to Seoul and back over the weekend to sort out a major problem of the bank with South Korean authorities over the weekend on site. “Sometimes I wake up in the morning in a hotel and have no clue as to where I am,” Ackermann once says. In a prime time feature on him for the German television network ARD, award-winning filmmaker Hubert Seipel describes the CEO of Deutsche Bank as a “restless global salesman of capital”. No wonder: While once 80 percent of his bank’s business was domestic, its vast majority meanwhile is abroad.

In the past years, the institution has seen especially swift growth in the booming region of Asia where it has joined the league of leading financial institutions, just as it previously did in Europe and the US. It has branch offices in 17 Asian countries. Since 2008, when it posted two billion euros in net revenues from the Far East (excluding Japan), that figure has more than doubled. The bank has been involved in many of the biggest IPOs in the region. All this requires the CEO to travel a lot.

Unlike most top managers in the Frankfurt financial community, the globetrotting Deutsche Bank boss does not live in a posh mansion on the slopes of the Taunus mountains overlooking the bank towers in the distance, but in a four-room rental apartment near Palmengarten in the Westend section of downtown Frankfurt. Ackermann prefers “the cosmos of a multinational urban society” to a shielded life behind high hedges and walls as Hilmar Hoffmann, former head of cultural affairs in the city government, puts it in the chapter of his book on famous Frankfurt citizen (Die großen Frankfurter) devoted to the Swiss national.

Ackermann’s decision for an apartment downtown had been made for mainly practical reasons, however. He simply has no use for a mansion in prestigious Kronberg. Even his apartment shows: Nobody really lives there. It is just a place to stay, a pied-à-terre, as the French so aptly call such temporary lodgings. The furnishings are understated and practical. The only item that catches the eye is a Swiss landscape painting by Ernst-Ludwig Kirchner in the hallway.

Ackermann spends as little time in his apartment on Siesmayerstraße as he does at his office on the 32nd floor of the A-Tower of Deutsche Bank HQ at Taunusanlage. His desk there is always cleared off and empty except for a few folders of documents to sign. The run-of-the-mill furniture, glass tables and black leather chairs, is the kind one can also find in the office of a director of a small savings and loan. The wall shelf is full of odds and ends: a three-mast schooner in a bottle as a keepsake of a visit to Hamburg, a statuette of the Greek goddess Nike as a memento of receiving an honorary doctorate from the Democritus University of Thrace and other souvenirs from his travels. The room is devoid of anything personal except the photos of his Finnish wife Pirkko, to whom he has been married for over 35 years, and their daughter Catherine, a trained actress and film producer.

A lacquered burl cigar box and a heavy crystal ashtray are the only striking items. Smoking is strictly prohibited throughout the towers, with one exception – the boss’s office. To prevent the sprinkler system there from being triggered when he occasionally lights a cigar, the sensitivity of the smoke detector has been reduced.

Josef Ackermann was never interested in a cozy or representative space for himself at Deutsche Bank headquarters. And why should he have been? He is hardly ever there and sets no store by appearances. In any case, he does not indulge in the kind of imposing and cocky displays so many bankers exhibit. His uniform is a well-tailored yet understated dark blue single-breasted suit without a pocket square, a mono-colored or subtly striped light blue or white shirt with cufflink sleeves and a conventional collar. Watch (an Omega), tie and cufflinks are of top quality but likewise unostentatious.

The Deutsche CEO is unpretentious in demeanor. He carries his black calfskin briefcase himself and travels without an entourage of assistants. He does not pay with a black or platinum creditcard, the Gold Mastercard suits him just fine. If he gets hungry late at night after not having had a proper meal all day, his favorite items to order at the hotel bar are a glass of house red and curry sausage with fries. At the office, his secretaries always make sure one drawer is well stocked with Toblerone chocolate bars from his home country.

Josef Ackermann’s interest, ambition and vanity have a different focus. His most remarkable trait is that he always wants to be a step ahead, to prove superior, to know more than everyone else around him, and everything with greater precision.

This insistence may get on the nerves of his entourage, but it also means that Ackermann never forgot how to listen, unlike so many others in similar positions. In any event, this trait was of pivotal importance in my decision to join Deutsche Bank. And it soon turned out that I had not been mistaken.

A few weeks after I started working in Frankfurt, Ackermann takes part in a panel discussion at the annual meeting of the Swiss Industrial Association in Zurich. He comes across as impatient and sharp with one of his fellow panelists. When I tell him so afterwards and recommend he not flaunt his intellectual superiority, he does not sweep my criticism gruffly aside but starts a discussion instead and explains his behavior: the woman’s arguments had bored him. Boredom is something he cannot handle well I find out that way. It lets his concentration and discipline wane – and he makes mistakes.

Josef Ackermann the banker is driven not by greed but by curiosity, especially about people. The more important they are, the better. The encounters with them on his travels around the globe flatter his ego and let him find out how he measures up to them. They allow him to prepare the ground for big deals and mandates, to soak up information he could use for the benefit of the bank. Josef Ackermann banks on his countless contacts with stockholders, customers, rulers, regulators, and employees to gain greater insights. No distance is too far for him, nothing too much or too exhausting. Nowhere, as I later observe on many joint trips with him, is he more in touch with himself than ‘on the road’. A colonel in the reserves of the Swiss Armed Forces, Ackermann clearly prefers the front to the base.

It was not until he took command that Deutsche Bank became a truly global, multicultural institution. Under his leadership the bank grew to be represented in more than 70 countries with a highly diverse work force from nearly 150 countries bound together by English as the common corporate language and by the motto “Passion to Perform”. When Ackermann first started in Frankfurt, he tells me early on in my time at the bank, German was the official language at the annual leadership conference of the 100-plus top executives of the bank and a German actress named Hannelore Elsner recited poems in the language of her home country.

The Deutsche Bank CEO’s international network is unparalleled. He is on the board of trustees of the World Economic Forum in Davos, member of the steering committee of the Bilderberg conference and chairs the economic advisory board of the Goethe Institute, the German government’s global cultural institution. In business, he knows everyone who is anyone, worldwide. And he is almost as well-connected when it comes to politics. The VIPs he frequents range from various US presidents to the heads of state and government of Russia and China, from the oil sheiks in Arabia to the crowned heads of Europe.

He discusses the US legal system with George W. Bush in the Oval Office and the best possible financial system for Russia with Vladimir Putin at the latter’s residence in Novo-Ogaryovo at the outskirts of Moscow. He explains the dangers of the European sovereign debt crisis to Spanish King Juan Carlos on a visit to the royal palace in Madrid. On the farm of fabulously wealthy prince and big-time investor Al-Waleed bin Talal al Saud in the Saudi Arabian desert, Ackermann plays foosball with the prince’s wife with such passion that he gets blisters on his hands and has to have a doctor bandage him up. Wang Qishan, the former mayor of Beijing and later vice-premier, on an official trip to Europe stops in Frankfurt for a joint meal of osso bucco, his favorite western dish, with Josef Ackermann at Villa Sander, the guesthouse of Deutsche Bank.

I once asked my boss which of the many prominent figures he knows had impressed him most. After pondering for a moment, he cites Jiang Zemin, the former Chinese head of state. Jiang’s profound knowledge of European culture had put him to shame: “What Western head of state or government or company CEO can recite a Chinese poem or sing a Chinese folk song?” says Ackermann. Western politicians and businesspeople should learn much more about the culture of this vast empire to be on an equal footing. “The Chinese know us much better than we know them.”

Wherever the German chancellor or foreign minister goes, the Deutsche CEO has been there before. And it is not rare for his discussion partners to send him on his way with a message for the government in Berlin. This network and the perception of his being a representative of Germany is an invaluable asset for Deutsche Bank. As a consequence, its reputation in the world is much greater than its value on the stock market. They also prove to be a huge plus when it comes to coping with and working through the financial crisis.

The myriad observations and ideas Ackermann gathers on his trips are systematically fed into his organization. Sometimes while still on the road or at the latest on returning home. His office has two secretaries and two executive assistants who are always on their toes even when the boss is gone. His schedule is so tight day after day and usually months in advance that one elevator down to the parking garage in the basement of the bank is routinely blocked for the CEO as soon as he sets off for his next appointment or enters the garage on his return. He does not have a minute to waste. Mathias Fluck, Ackermann’s chauffeur, admires his boss for the “absolute reliability” he displays. “He is always on time – like a Swiss watch,” Fluck says.

Josef Ackermann prefers oral communication. There is virtually nothing from him in writing. E-mail is taboo. A brief “OK,” “pls discuss” or “pls call!” on paper or as a text message – that is it.

The boss runs the bank by numbers. At all times he is fully up-to-date on how business is going. Every day around 4 p. m. Central European Time he receives the so-called flash, one page with the current key figures from the individual business divisions. Nothing essential escapes his eagle eye. On detecting a shortcoming, he would immediately pick up the phone and take direct and, if need be, hard countermeasures to remedy it.

By contrast, if everything is going smoothly, Josef Ackermann gives people free rein. He is no micromanager but a perfectionist, satisfied with nothing short of the best, regardless of how many rounds have to be made to achieve it. He is not a workaholic but someone who lives his role to the fullest. In addition, he has a razor-sharp mind, the memory of an elephant, and the constitution of an ox.

Leisure time is a foreign concept to the Deutsche CEO. He gets little respite from his grueling schedule with 80 to 100 hour weeks nearly without a break, irregular meals, little sleep and often changing time zones. Three weeks of summer vacation in his country home in the Southern Swiss canton of Ticino, an occasional night at the opera, a visit to an art museum or a game at the Frankfurt soccer stadium since the local club Eintracht Frankfurt has returned to the top league, a brisk walk through the woods on the weekends at home in Zurich or around the block when on the road have to suffice. Private side-trips such as his weekend excursion to the Cape of Good Hope in late June 2010 are extremely rare.

Josef Ackermann pays a short visit to the FIFA World Cup in South Africa to join customers in attending the soccer match Brazil vs. Portugal at Moses Mabhida Stadium in Durban. He then takes part in the Fortune 500 Global Forum where CEOs from the world’s largest companies meet every year. In 2010 the organizers have picked Cape Town as the venue because of the World Cup competition.

Friday afternoon, as we are having a cappuccino on the lush park terrace of the venerable Mount Nelson Hotel at the foot of Table Mountain, Ackermann spontaneously suggests going on a private outing the next day. First, he wants to visit a game reserve to see the Big Five, the five animals considered especially difficult and dangerous to hunt. Then, before returning for the closing event of the conference on Saturday evening, he wants to see the Cape of Good Hope.

The game reserve is a few hours’ drive from Cape Town so we leave the hotel in the middle of the night to reach it by dawn. The chances of seeing the animals in the wild are highest early in the morning. We are rewarded for our early rising and fortune is on our side. We catch sight of buffalo, elephant, lion, and rhinoceros at close range. Only a leopard is nowhere in sight. But two giraffes let us watch them munching breakfast instead.

Next we proceed to the Cape of Good Hope. On the rocky cliffs that have spelled doom to many a sailing ship on its way to India in past centuries, we can observe the results of piracy on the Horn of Africa at the opposite end of the black continent. Container ships are passing by on the horizon almost lined up like pearls on a necklace. After years of being abandoned, the long route around Africa appears to pay off again.

When travelling abroad Ackermann is usually without any security personnel, the bodyguard constantly at his side in South Africa is an exception. In Germany, two bodyguards accompany him almost everywhere he goes. Since the Mannesmann trial, he is among the most endangered persons in the republic. His company limousine, a Mercedes S-Class, is heavily armored. So much so that I always need both hands to open the left rear door when getting in and out of the car.

For safety reasons and to be able to handle his immense workload, the Deutsche CEO regularly uses the services of NetJets, the private plane leasing company from the empire of US star investor Warren Buffett. While in the air, Ackermann has his Gulfstream or Falcon jet all to himself and his phone is quiet. He uses the time for uninterrupted reflection, studying documents or personally perusing a newspaper or magazine for a change. His favorites: The Financial Times and The Economist.

To keep my boss informed at all times about everything important in the media, every morning before 8 o’clock Central European Time (an hour later on weekends) I send him a text message with a summary of national and international coverage on Deutsche Bank. Over time, a mix of German and English abbreviations intelligible only to the two of us emerges. Afterwards, we talk five to ten minutes on the phone – or longer on weekends. During the day, Ackermann receives updates and we get on the phone again – also about current inquiries from journalists. Before appointments, he usually contacts me to ask about the latest news: “Anything else happen?” That way the Deutsche CEO is constantly up to date and fully aware of the issues of special interest to the media at any given time. In turn, the communication department at the bank is always promptly informed about all relevant facts and about the management’s views on current issues and able to speedily and competently respond to media inquiries.

In my briefings, I do not omit negative news or wrap it in cotton candy. On the contrary, I ususally give it greater weight than the positive news and also express my personal opinion without reservations. Ackermann appreciates straight talk – he is a straight talker himself, and loathes whitewashing, dishonesty, and evasion. A culture of open constructive debate is a vital principle of management for him.

Before I began working at Deutsche Bank, he had told me that his approach was “Don’t shoot the messenger.” As I later found out, the messenger is not shot but he certainly is grilled. He always has to give plausible reasons for the bad news. And he is expected to have solutions on hand regarding how that kind of bad news can be avoided in the future. During the financial crisis telling the truth often means telling an unpleasant truth. Every time when stress builds up to another peak, I keep asking myself how many people in the bank are deliberately avoiding this stress.